As part of this interview, Satya Nadella gave Dylan Patel (founder of SemiAnalysis) and me an exclusive first-look at their brand-new Fairwater 2 datacenter.

Microsoft is building multiple Fairwaters, each of which has hundreds of thousands of GB200s & GB300s. Between all these interconnected buildings, they’ll have over 2 GW of total capacity. Just to give a frame of reference, even a single one of these Fairwater buildings is more powerful than any other AI datacenter that currently exists.

Satya then answered a bunch of questions about how Microsoft is preparing for AGI across all layers of the stack.

Watch on YouTube; listen on Apple Podcasts or Spotify.

Sponsors

Labelbox produces high-quality data at massive scale, powering any capability you want your model to have. Whether you’re building a voice agent, a coding assistant, or a robotics model, Labelbox gets you the exact data you need, fast. Reach out at labelbox.com/dwarkesh

CodeRabbit automatically reviews and summarizes PRs so you can understand changes and catch bugs in half the time. This is helpful whether you’re coding solo, collaborating with agents, or leading a full team. To learn how CodeRabbit integrates directly into your workflow, go to coderabbit.ai/dwarkesh

To sponsor a future episode, visit dwarkesh.com/advertise.

Timestamps

(00:03:20) - Business models for AGI

(00:20:02) - Whose margins will expand most?

(00:47:47) - The hyperscale business

(01:02:44) - In-house chip & OpenAI partnership

(01:09:35) - The CAPEX explosion

(01:15:07) - Will the world trust US companies to lead AI?

Transcript

00:00:00 - Fairwater 2

Dwarkesh Patel 00:00:00

Today we are interviewing Satya Nadella. “We” being me and Dylan Patel, who is founder of SemiAnalysis. Satya, welcome.

Satya Nadella 00:00:07

Thank you. It’s great. Thanks for coming over to Atlanta.

Dwarkesh Patel 00:00:10

Thank you for giving us the tour of the new facility. It’s been really cool to see.

Satya Nadella 00:00:13

Absolutely.

Dwarkesh Patel 00:00:15

Satya and Scott Guthrie, Microsoft’s EVP of Cloud and AI, give us a tour of their brand new Fairwater 2 data center, the current most powerful in the world.

Scott Guthrie 00:00:25

We’ve tried to 10x the training capacity every 18 to 24 months. So this would effectively be a 10x increase from what GPT-5 was trained with. So to put it in perspective in the number of optics, the network optics in this building is almost as much as all of Azure across all our data centers two and a half years ago.

Satya Nadella 00:00:44

It’s got like five million network connections.

Dwarkesh Patel 00:00:47

You’ve got all this bandwidth between different sites in a region and between the two regions. So is this like a big bet on scaling in the future, that you anticipate in the future that there’s going to be some huge model that will require two whole different regions to train?

Satya Nadella 00:00:59

The goal is to be able to aggregate these flops for a large training job and then put these things together across sites. The reality is you’ll use it for training and then you’ll use it for data gen, you’ll use it for inference in all sorts of ways. It’s not like it’s going to be used only for one workload forever.

Scott Guthrie 00:01:20

Fairwater 4, which you’re going to see under construction nearby, will also be on that one petabit network so that we can actually link the two at a very high rate. Then we do the AI WAN connecting to Milwaukee where we have multiple other Fairwaters being built.

Satya Nadella 00:01:35

Literally you can see the model parallelism and the data parallelism. It’s kind of built for, essentially, the training jobs, the super pods across this campus. And then with the WAN, you can go to the Wisconsin data center. You literally run a training job with all of them getting aggregated.

Scott Guthrie 00:02:00

What we’re seeing right here is a cell with no servers in it yet, no racks.

Dylan Patel 00:02:04

How many racks are in a cell?

Scott Guthrie 00:02:06

We don’t necessarily share that per se, but…

Dylan Patel 00:02:10

That’s the reason I ask.

Scott Guthrie 00:02:12

You’ll see upstairs.

Dylan Patel 00:02:14

I’ll start counting.

Scott Guthrie 00:02:15

You can start counting. We’ll let you start counting.

Dylan Patel 00:02:16

How many cells are there in this building?

Scott Guthrie 00:02:17

That part also I can’t tell you.

Dwarkesh Patel 00:02:19

Well, division is easy, right?

Satya Nadella 00:02:24

My God, it’s kind of loud.

Dwarkesh Patel 00:02:27

Are you looking at this like, “Now I see where my money is going.”

Satya Nadella 00:02:30

It’s like, “I run a software company. Welcome to the software company.”

Dwarkesh Patel 00:02:35

How big is the design space once you’ve decided to use the GB200s and the NVLink? How many other decisions are there to be made?

Satya Nadella 00:02:41

There is coupling from the model architecture to what is the physical plan that’s optimized. And it’s also scary in that sense, which is, there’s going to be a new chip that’ll come out. Take Vera Rubin Ultra. That’s going to have power density that’s going to be so different, with cooling requirements that are going to be so different. So you kind of don’t want to just build all to one spec. That goes back a little bit to the dialogue we’ll have, which is that you want to be scaling in time as opposed to scale once and then be stuck with it.

00:03:20 - Business models for AGI

Dylan Patel 00:03:20

When you look at all the past technological transitions—whether it be railroads or the Internet or replaceable parts, industrialization, the cloud, all of these things—each revolution has gotten much faster in the time it goes from technology discovered to ramp and pervasiveness through the economy. Many folks who have been on Dwarkesh’s podcast believe this is the final technological revolution or transition, and that this time is very, very different.

At least so far in the markets, in three years we’ve already skyrocketed to hyperscalers doing $500 billion of capex next year, which is a scale that’s unmatched to prior revolutions in terms of speed. The end state seems to be quite different. Your framing of this seems quite different from what I would call the “AI bro” who’s like, “AGI is coming.” I’d like to understand that more.

Satya Nadella 00:04:17

I start with the excitement that I also feel for the idea that maybe after the Industrial Revolution this is the biggest thing. I start with that premise. But at the same time, I’m a little grounded in the fact that this is still early innings. We’ve built some very useful things, we’re seeing some great properties, these scaling laws seem to be working. I’m optimistic that they’ll continue to work. Some of it does require real science breakthroughs, but it’s also a lot of engineering and what have you.

That said, I also sort of take the view that even what has been happening in the last 70 years of computing has also been a march that has helped us move. I like one of the things that Raj Reddy has as a metaphor for what AI is. He’s a Turing Award winner at CMU. He had this, even pre-AGI. He had this metaphor for AI, it should either be a guardian angel or a cognitive amplifier. I love that. It’s a simple way to think about what this is. Ultimately, what is its human utility? It is going to be a cognitive amplifier and a guardian angel. If I view it that way, I view it as a tool.

But then you can also go very mystical about it and say this is more than a tool. It does all these things, which only humans did before so far. But that has been the case with many technologies in the past. Only humans did a lot of things, and then we had tools that did them.

Dwarkesh Patel 00:05:56

We don’t have to get wrapped up in the definition here, but one way to think about it is, maybe it takes five years, ten years, twenty years. At some point, eventually a machine is producing Satya tokens, and the Microsoft board thinks that Satya tokens are worth a lot.

Dylan Patel 00:06:10

How much are you wasting of this economic value by interviewing Satya?

Dwarkesh Patel 00:06:15

I could not afford the API costs of Satya tokens. Whatever you want to call it, are the Satya tokens a tool or an agent, whatever. Right now, if you have models that cost on the order of dollars or cents per million tokens, there’s just an enormous room for margin expansion there, where a million tokens of Satya are worth a lot. Where does that margin go and what level of that margin is Microsoft involved in is the question I have.

Satya Nadella 00:06:45

In some sense this goes back again to, essentially, what’s the economic growth picture going to really look like? What’s the firm going to look like? What’s productivity going to look like? That to me is where, again, if the Industrial Revolution created… After 70 years of diffusion is when you started seeing the economic growth. That’s the other thing to remember. Even if the tech is diffusing fast this time around, for true economic growth to appear it has to diffuse to a point where the work, the work artifact, and the workflow has to change. So that’s one place where I think the change management required for a corporation to truly change is something we shouldn’t discount.

Going forward, do humans and the tokens they produce get higher leverage, whether it’s the Dwarkesh or the Dylan tokens of the future? Think about the amount of technology. Would you be able to run SemiAnalysis or this podcast without technology? No chance, at the scale that you have been able to achieve, there’s no chance.

So the question is, what’s that scale? Is it going to be 10x’ed with something that comes through? Absolutely. Therefore, whether you’re ramped to some revenue number or you’re ramped to some audience number or what have you, that I think is what’s going to happen. The point is, what took 70 years, maybe 150 years for the Industrial Revolution, may happen in 20 years, 25 years. I would love to compress what happened in 200 years of the Industrial Revolution into a 20-year period, if we’re lucky.

Dylan Patel 00:08:28

Microsoft historically has been perhaps the greatest software company, the largest software-as-a-service company. You’ve gone through a transition in the past where you used to sell Windows licenses and disks of Windows or Microsoft, and now you sell subscriptions to 365.

As we go from that transition to where your business is today, there’s also a transition going on after that. Software-as-a-service has incredibly low incremental cost per user. There’s a lot of R&D, there’s a lot of customer acquisition costs. This is sort of why, not Microsoft, but the SaaS companies have underperformed massively in the markets, because the COGS of AI is just so high, and that just completely breaks how these business models work.

How do you, as perhaps the greatest software-as-a-service company, transition Microsoft to this new age where COGS matters a lot and the incremental cost per user is different? Because right now you’re charging like, “Hey, it’s 20 bucks for Copilot.”

Satya Nadella 00:09:29

It’s a great question because in some sense with the business models themselves, the levers are going to remain similar. If you look at the menu of models starting from consumer all the way, there will be some ad unit, there will be some transaction, there will be some device gross margin for somebody who builds an AI device. There will be subscriptions, consumer and enterprise, and then there’ll be consumption. So I still think those are all the meters.

To your point, what is a subscription? Up to now, people like subscriptions because they can budget for them. They are essentially entitlements to some consumption rights that come encapsulated in a subscription. So I think that in some sense becomes a pricing decision. How much consumption you are entitled to is, if you look at all the coding subscriptions, kind of what they are, right? Then you have the pro tier, the standard tier, and what have you. So I think that’s how the pricing and the margin structures will get tiered.

The interesting thing is that at Microsoft, the good news for us is we are in that business across all those meters. At a portfolio level, we pretty much have consumption, subscriptions, to all of the other consumer levers as well. I think time will tell which of these models make sense in what categories.

One thing on the SaaS side, since you brought it up, which I think a lot about. Take Office 365 or Microsoft 365. Having a low ARPU is great, because here’s an interesting thing. During the transition from server to cloud, one of the questions we used to ask ourselves is, “Oh my God, if all we did was just basically move the same users who were using our Office licenses and our Office servers at the time to the cloud, and we had COGS, this is going to not only shrink our margins but we’ll be fundamentally a less profitable company.”

Except what happened was the move to the cloud expanded the market like crazy. We sold a few servers in India, we didn’t sell much. Whereas in the cloud suddenly everybody in India also could afford fractionally buying servers, the IT cost. In fact, the biggest thing I had not realized, for example, was the amount of money people were spending buying storage underneath SharePoint. In fact, EMC’s biggest segment may have been storage servers for SharePoint. All that sort of dropped in the cloud because nobody had to go buy. In fact, it was working capital, meaning basically, it was cash flow out. So it expanded the market massively.

So this AI thing will be that. If you take coding, what we built with GitHub and VS Code over decades, suddenly the coding assistant is that big in one year. That I think is what’s going to happen as well, which is the market expands massively.

00:12:48 - Copilot

Dwarkesh Patel 00:12:48

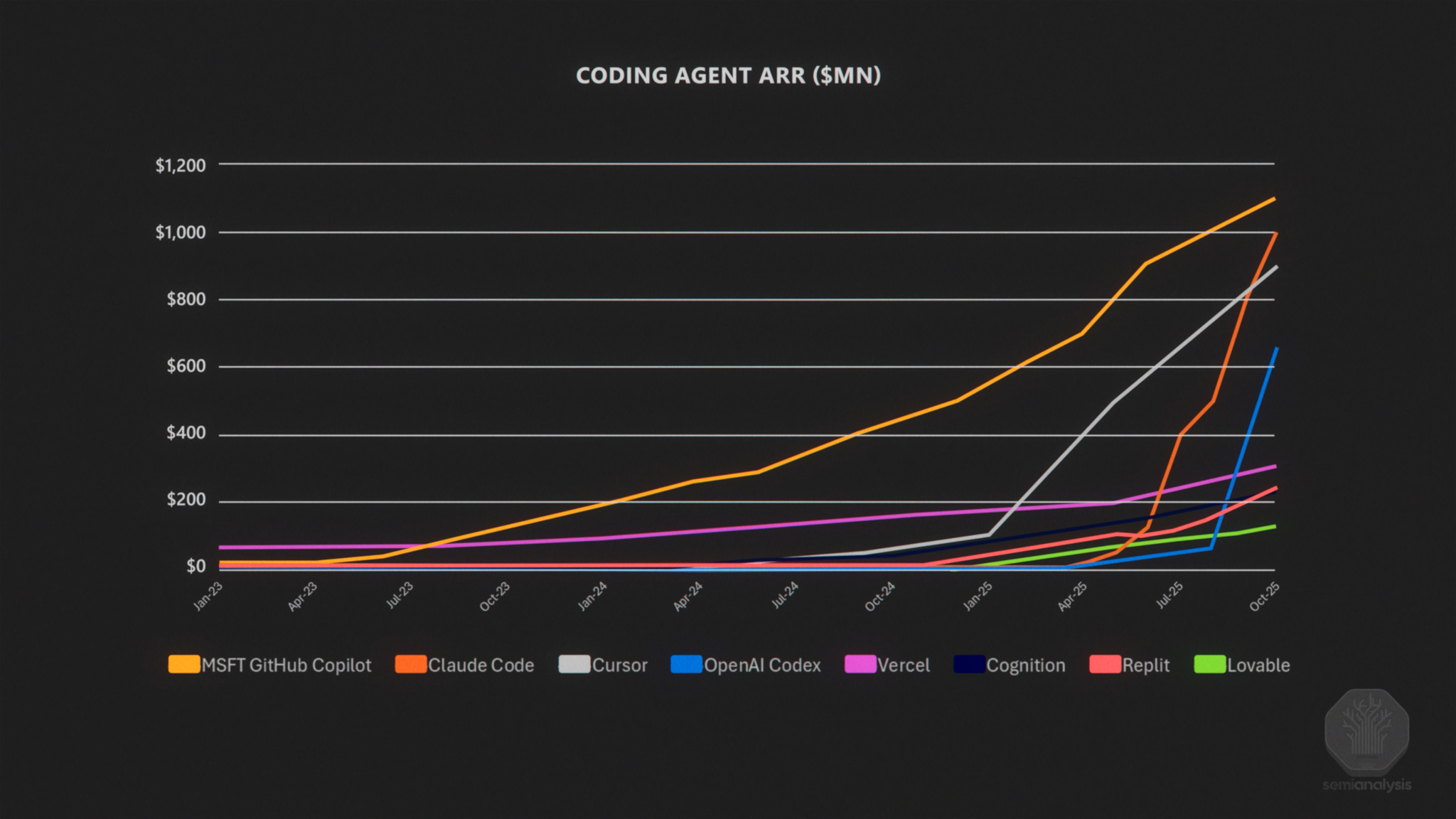

There’s a question of, the market will expand, but will the parts of the revenue that touch Microsoft expand? Copilot is an example. If you look earlier this year, according to Dylan’s numbers, GitHub Copilot revenue was like $500 million or something like that and there were no close competitors. Whereas now you have Claude Code, Cursor, and Copilot with around similar revenue, around a billion. Codex is catching up around $700–800 million. So the question is, across all the surfaces that Microsoft has access to, what is the advantage that Microsoft’s equivalents of Copilot have?

Satya Nadella 00:13:25

By the way, I love this chart.

I love this chart for so many reasons. One is we’re still on the top. Second is all these companies that are listed here are all companies that have been born in the last four or five years. That to me is the best sign. You have new competitors, new existential problems. When you say, who’s it now? Claude’s going to kill you, Cursor is going to kill you, it’s not Borland. Thank God. That means we are in the right direction.

This is it. The fact that we went from nothing to this scale is the market expansion. This is like the cloud-like stuff. Fundamentally, this category of coding and AI is probably going to be one of the biggest categories. It is the software factory category. In fact, it may be bigger than knowledge work. I want to keep myself open-minded about it.

We’re going to have tough competition. That’s your point, which is a great one. But I’m glad we have parlayed what we had into this and now we have to compete. On the competing side, even in the last quarter we just finished, we did our quarterly announcement and I think we grew from 20 to 26 million subs. I feel good about our sub growth and where the direction of travel on that is.

But the more interesting thing that has happened is, guess where all the repos of all these other guys who are generating lots and lots of code go? They go to GitHub. GitHub is at an all-time high in terms of repo creation, PRs, everything. In some sense we want to keep that open, by the way. That means we want to have that. We don’t want to conflate that with our own growth. Interestingly enough, we are getting one developer joining GitHub a second or something, that is the stat, I think. And 80% of them just fall into some GitHub Copilot workflow, just because there are. By the way, many of these things will even use some of our coding code review agents, which are by default on, just because you can use it. We’ll have many, many structural shots at this. The thing that we’re also going to do is what we did with Git. The primitives of GitHub, starting with Git, to issues, to actions, these are powerful, lovely things because they kind of are all built around your repo. We want to extend that.

Last week at GitHub Universe, that’s kind of what we did. We said Agent HQ was the conceptual thing that we said we’re going to build out. This is where, for example, you have a thing called Mission Control. You go to Mission Control, and now I can fire off. Sometimes I describe it as the cable TV of all these AI agents because I’ll have, essentially packaged into one subscription, Codex, Claude, Cognition stuff, anyone’s agents, Grok, all of them will be there. So I get one package and then I can literally go issue a task and steer them so they’ll all be working in their independent branches. I can monitor them. I think that’s going to be one of the biggest places of innovation, because right now I want to be able to use multiple agents. I want to be able to then digest the output of the multiple agents. I want to be able to then keep a handle on my repo.

If there’s some kind of a heads-up display that needs to be built and then for me to quickly steer and triage what the coding agents have generated, that to me, between VS Code, GitHub, and all of these new primitives we’ll build as Mission Control with a control plane. Observability… Just think about everyone who is going to deploy all this. It will require a whole host of observability of what agent did what at what time to what code base. I feel that’s the opportunity.

At the end of the day your point is well taken, which is we better be competitive and innovate. If we don’t, we will get toppled. But I like the chart, at least as long as we’re on the top, even with competition.

Dylan Patel 00:17:26

The key point here is sort of that GitHub will keep growing regardless of whose coding agent wins. But that market only grows at say 10, 15, 20%, which is way above GDP. It’s a great compounder. But these AI coding agents have grown from say $500 million run rate at the end of last year—which was just GitHub Copilot—to now where the current run rate across GitHub Copilot, Claude Code, Cursor, Cognition, Windsurf, Replit, OpenAI Codex… That’s run rating at $5–6 billion now for the Q4 of this year. That’s 10x.

When you look at the TAM of software agents, is it the $2 trillion of wages you pay people, or is it something beyond that? Because every company in the world will now be able to develop software more? No question Microsoft takes a slice of that. But you’ve gone from near 100%, or certainly way above 50%, to sub-25% market share in just one year. What is the confidence that people can get that Microsoft will keep winning?

Satya Nadella 00:18:30

It goes back a little bit, Dylan, to that there’s no birthright here, that we should have any confidence other than to say we should go innovate. Knowing the lucky break we have, in some sense, is that this category is going to be a lot bigger than anything we had high share in. Let me say it that way. You could say we had high share in VS Code, we had high share in the repos with GitHub, and that was a good market. But the point is that even having a decent share in what is a much more expansive market…

You could say we had a high share in client-server server computing. We have much lower share than that in hyperscale. But is it a much bigger business? By orders of magnitude. So at least it’s existence proof that Microsoft has been okay even if our share position has not been as strong as it was, as long as the markets we are competing in are creating more value. And there are multiple winners. That’s the stuff.

But I take your point that ultimately it all means you have to get competitive. I watch that every quarter. That’s why I’m very optimistic about what we’re going to do with Agent HQ, turning GitHub into a place where all these agents come. As I said, we’ll have multiple shots on goal on there. It need not be… Some of these guys can succeed along with us, so it doesn’t need to be just one winner and one subscription.

00:20:02 - Whose margins will expand most?

Dwarkesh Patel 00:20:02

I guess the reason to focus on this question is that it’s not just about GitHub, but fundamentally about Office and all the other software that Microsoft offers. One vision you could have about how AI proceeds is that the models are going to keep being hobbled and you’ll need this direct visible observability all the time.

Another vision is that over time these models which are now doing tasks that take two minutes, in the future, they’ll be doing tasks that take 10, 30 minutes. In the future, maybe they’re doing days worth of work autonomously. Then the model companies are charging thousands of dollars maybe for access to, really, a coworker which could use any UI to communicate with their human and migrate between platforms.

If we’re getting closer to that, why aren’t the model companies that are just getting more and more profitable, the ones that are taking all the margin? Why is the place where the scaffolding happens, which becomes less and less relevant as the AI becomes more capable, going to be that important? That goes to Office as it exists now versus coworkers that are just doing knowledge work.

Satya Nadella 00:21:07

That’s a great point. Does all the value migrate just to the model? Or does it get split between the scaffolding and the model? I think that time will tell. But my fundamental point also is that the incentive structure gets clear. Let’s take information work, or take even coding. Already in fact, one of my favorite settings in GitHub Copilot is called auto, which will just optimize. In fact I buy a subscription and the auto one will start picking and optimizing for what I am asking it to do. It could even be fully autonomous. It could arbitrage the tokens available across multiple models to go get a task done.

If you take that argument, the commodity there will be models. Especially with open source models, you can pick a checkpoint and you can take a bunch of your data and you’re seeing it. I think all of us will start, whether it’s from Cursor or from Microsoft, seeing some in-house models even. And then you’ll offload most of your tasks to it.

So one argument is if you win the scaffolding—which today is dealing with all the hobbling problems or the jaggedness of these intelligence problems, which you kind of have to—if you win that, then you will vertically integrate yourself into the model just because you will have the liquidity of the data and what have you. There are enough and more checkpoints that are going to be available. That’s the other thing.

Structurally, I think there will always be an open source model that will be fairly capable in the world that you could then use, as long as you have something that you can use that with, which is data and a scaffolding. I can make the argument that if you’re a model company, you may have a winner’s curse. You may have done all the hard work, done unbelievable innovation, except it’s one copy away from that being commoditized. Then the person who has the data for grounding and context engineering, and the liquidity of data can then go take that checkpoint and train it. So I think the argument can be made both ways.

Dylan Patel 00:23:36

Unpacking what you said, there’s two views of the world. One is that there are so many different models out there. Open source exists. There will be differences between the models that will drive some level of who wins and who doesn’t. But the scaffolding is what enables you to win.

The other view is that, actually, models are the key IP. And everyone’s in a tight race and there’s some, “Hey, I can use Anthropic or OpenAI.” You can see this in the revenue charts. OpenAI’s revenue started skyrocketing once they finally had a code model with similar capabilities to Anthropic, although in different ways.

There’s the view that the model companies are the ones that garner all the margin. Because if you look across this year, at least at Anthropic, their gross margins on inference went from well below 40% to north of 60% by the end of the year. The margins are expanding there despite more Chinese open source models than ever. OpenAI is competitive, Google is competitive, X/Grok is now competitive. All these companies are now competitive, and yet despite this, the margins have expanded at the model layer significantly. How do you think about that?

Satya Nadella 00:24:43

It’s a great question. Perhaps a few years ago people were saying, “Oh, I could just wrap a model and build a successful company.” That has probably gotten debunked just because of the model capabilities, and the tools used, in particular.

But the interesting thing is, when I look at Office 365, let’s take even this little thing we built called Excel Agent. It’s interesting. Excel Agent is not a UI-level wrapper. It’s actually a model that is in the middle tier. In this case, because we have all the IP from the GPT family, we are taking that and putting it into the core middle tier of the Office system to teach it what it means to natively understand Excel, everything in it. It’s not just, “Hey, I just have a pixel-level understanding.” I have a full understanding of all the native artifacts of Excel. Because if you think about it, if I’m going to give it some reasoning task, I need to even fix the reasoning mistakes I make. That means I need to not just see the pixels, I need to be able to see, “Oh, I got that formula wrong,” and I need to understand that.

To some degree, that’s all being done not at the UI wrapper level with some prompt, but it’s being done in the middle tier by teaching it all the tools of Excel. I’m giving it essentially a markdown to teach it the skills of what it means to be a sophisticated Excel user. It’s a weird thing that it goes back a little bit to the AI brain. You’re building not just Excel, business logic in its traditional sense. You’re taking the Excel business logic in the traditional sense and wrapping essentially a cognitive layer to it, using this model which knows how to use the tool. In some sense, Excel will come with an analyst bundled in and with all the tools used. That’s the type of stuff that will get built by everybody.

So even for the model companies, they’ll have to compete. If they price stuff high, guess what, if I’m a builder of a tool like this, I’ll substitute you. I may use you for a while. So as long as there’s competition… There’s always a winner-take-all thing. If there’s going to be one model that is better than everybody else with massive distance, yes, that’s a winner-take-all. But as long as there’s competition where there are multiple models, just like hyperscale competition, and there’s an open source check, there is enough room here to go build value on top of models.

At Microsoft, the way I look at it is that we are going to be in the hyperscale business, which will support multiple models. We will have access to OpenAI models for seven more years, which we will innovate on top of. Essentially, I think of ourselves as having a frontier-class model that we can use and innovate on with full flexibility. And we’ll build our own models with MAI. So we will always have a model level. And then we’ll build—whether it’s in security, whether it’s in knowledge work, whether it’s in coding, or in science—our own application scaffolding, which will be model-forward. It won’t be a wrapper on a model, but the model will be wrapped into the application.

Dwarkesh Patel 00:28:04

I have so many questions about the other things you mentioned. But before we move onto those topics, I still wonder whether this is not forward-looking on AI capabilities, where you’re imagining models like they exist today. It takes a screenshot of your screen, but it can’t look inside each cell and what the formula is. I think the better mental model here is just imagining that these models will be able to use a computer as well as a human. A human knowledge worker who is using Excel can look into the formulas, can use alternative software, can migrate data between Office 365 and another piece of software if the migration is necessary, et cetera.

Satya Nadella 00:28:43

That’s kind of what I’m saying.

Dwarkesh Patel 00:28:45

But if that’s the case, then the integration with Excel doesn’t matter that much.

Satya Nadella 00:28:48

No, no, don’t worry about the Excel integration. After all, Excel was built as a tool for analysts. Great. So whoever is this AI that is an analyst should have tools that they can use.

Dwarkesh Patel 00:29:03

They have the computer. Just the way a human can use a computer. That’s their tool.

Satya Nadella 00:29:05

The tool is the computer. So all I’m saying is that I’m building an analyst as essentially an AI agent, which happens to come with an a priori knowledge of how to use all of these analytical tools.

Dwarkesh Patel 00:29:20

Just to make sure we’re talking about the same thing, is it a thing that a human like me using Excel…

Satya Nadella 00:29:30

No, it’s completely autonomous. So we should now maybe lay out what I think the future of the company is. The future of the company would be the tools business in which I have a computer, I use Excel. In fact, in the future I’ll even have a Copilot, and that Copilot will also have agents. But it’s still me steering everything, and everything is coming back. That’s one world.

The second world is the company just literally provisions a computing resource for an AI agent, and that is working fully autonomously. That fully autonomous agent will have essentially an embodied set of those same tools that are available to it. So this AI tool that comes in also has not just a raw computer, because it’s going to be more token-efficient to use tools to get stuff done.

In fact, I kind of look at it and say that our business, which today is an end-user tools business, will become essentially an infrastructure business in support of agents doing work. It’s another way to think about it. In fact, all the stuff we built underneath M365 still is going to be very relevant. You need some place to store it, some place to do archival, some place to do discovery, some place to manage all of these activities, even if you’re an AI agent. It’s a new infrastructure.

Dwarkesh Patel 00:31:00

To make sure I understand, you’re saying theoretically a future AI that has actual computer use—which all these model companies are working on right now—could use, even if it’s not partnered with Microsoft or under our umbrella, Microsoft software. But you’re saying, if you’re working with our infrastructure, we’re going to give them lower-level access that makes it more efficient for you to do the same things you could have otherwise done anyways?

Satya Nadella 00:31:24

100%. What happened is we had servers, then there was virtualization, and then we had many more servers. That’s another way to think about this. Don’t think of the tool as the end thing. What is the entire substrate underneath that tool that humans use? That entire substrate is the bootstrap for the AI agent as well, because the AI agent needs a computer.

In fact, one of the fascinating things where we’re seeing a significant amount of growth is all these guys who are doing these Office artifacts and what have you, as autonomous agents and so on want to provision Windows 365. They really want to be able to provision a computer for these agents. Absolutely. That’s why we’re going to have essentially an end-user computing infrastructure business, which is going to just keep growing because it’s going to grow faster than the number of users.

That’s one of the other questions people ask me, “Hey, what happens to the per-user business?” At least the early signs maybe, the way to think about the per-user business is not just per user, it’s per agent. And if you say it’s per user and per agent, the key is what’s the stuff to provision for every agent? A computer, a set of security things around it, an identity around it. All those things, observability and so on, are the management layers. That’s all going to get baked into that.

Dylan Patel 00:32:54

The way to frame it—at least the way I currently think about it and I’d like to hear your view—is that these model companies are all building environments to train their models to use Excel or Amazon shopping or whatever it is, book flights. But at the same time, they’re also training these models to do migration. Because that is probably the most immediately valuable thing: converting mainframe-based systems to standard cloud systems, converting Excel databases into real databases with SQL, or converting what is done in Word and Excel to something that is more programmatic and more efficient in a classical sense that can be done by humans as well. It’s just not cost-effective for the software developer to do that.

That seems to be what everyone is going to do with AI, for the next few years at least, to massively drive value. How does Microsoft fit into that if the models can utilize the tools themselves to migrate to something? Yes, Microsoft has a leadership position in databases and in storage and in all these other categories, but the use of an Office ecosystem is going to be significantly less just like the use of a mainframe ecosystem could be potentially less. Now mainframes have grown for the last two decades actually, even though no one talks about them anymore. They’ve still grown.

Satya Nadella 00:34:16

100%, I agree with that.

Dylan Patel 00:34:17

How does that flow?

Satya Nadella 00:34:18

At the end of the day, there is going to be a significant amount of time where there’s going to be a hybrid world, because people are going to be using the tools that are going to be working with agents that have to use tools, and they have to communicate with each other. What’s the artifact I generate that then a human needs to see? All of these things will be real considerations in any place, the outputs, inputs. I don’t think it’ll just be about, “Oh, I migrated off.” The bottom line is that I have to live in this hybrid world.

But that doesn’t fully answer your question because there can be a real new efficient frontier where it’s just agents working with agents and completely optimized. Even when agents are working with agents, what are the primitives that are needed? Do you need a storage system? Does that storage system need to have e-discovery? Do you need to have observability? Do you need to have an identity system that is going to use multiple models with all having one identity system? These are all the core underlying rails we have today for what are the Office systems or what have you. And that’s what we will have in the future as well.

You’ve talked about databases. I mean man, I would love all of Excel to have a database backend. I would love for all that to happen immediately. And that database is a good database. Databases in fact will be a big thing that will grow. If I think about all of the Office artifacts being structured better, the ability to do the joins between structured and unstructured better because of the agentic world, that will grow the underlying infrastructure business. It happens that the consumption of that is all being driven by agents.

You could say all that is just-in-time generated software by a model company. That could also be true. We will be one such model company too. We will build in... The competition could be that we will build a model plus all the infrastructure and provision it, and then there will be competition between a bunch of those folks who can do that.

00:36:17 - MAI

Dwarkesh Patel 00:36:17

Speaking of model companies, you say not only will you have the infrastructure, you’ll have the model itself. Right now, Microsoft AI’s most recent model that was released two months ago is 36 in Chatbot Arena. You obviously have the IP rights to OpenAI. To the extent you agree with that, it seems to be behind. Why is that the case, especially given the fact that you theoretically have the right to fork OpenAI’s monorepo or distill their models, especially if it’s a big part of your strategy that you need to have a leading model company?

Satya Nadella 00:36:51

First of all, we are absolutely going to use the OpenAI models to the maximum across all of our products. That’s the core thing that we’re going to continue to do all the way for the next seven years, and not just use it but then add value to it. That’s where the analyst and this Excel agent, these are all things that we will do where we’ll do RL fine-tuning. We’ll do some mid-training runs on top of a GPT family where we have unique data assets and build capability.

With the MAI model, the way that I think we’re going to think about it is that the good news here with the new agreement is we can be very, very clear that we’re going to build a world-class superintelligence team and go after it with a high ambition. But at the same time, we’re also going to use this time to be smart about how to use both these things. That means we will, on one end, be very product-focused, and on the other end, be very research-focused. Because we have access to the GPT family, the last thing I want to do is use my flops in a way that is just duplicative and doesn’t add much value.

I want to be able to take the flops that we use to generate a GPT family and maximize its value, while my MAI flops are being used for… Let’s take the image model that we launched, which I think is at number nine in the image arena. We’re using it both for cost optimization, it’s on Copilot, it’s in Bing, and we’re going to use that. We have an audio model in Copilot. It’s got personality and what have you. We optimized it for our product. So we will do those.

Even on the LMArena, we started on the text one and it debuted at like 13. By the way, it was done only on around 15,000 H100s. It was a very small model. So it was, again, to prove out the core capability, the instruction following, and everything else. We wanted to make sure we could match what was state of the art. That shows us, given scaling laws, what we are capable of doing if we gave more flops to it. The next thing we will do is an omni-model where we will take the work we have done in audio, what we have done in image, and what we have done in text. That will be the next pit stop on the MAI side.

So when I think about the MAI roadmap, we are going to build a first-class superintelligence team. We are going to continue to drop, and do it in the open, some of these models. They will either be used in our products, because they’re going to be latency-friendly, cost-friendly, or what have you, or they’ll have some special capability. And we will do real research in order to be ready for the next five, six, seven, eight breakthroughs that are all needed on this march towards superintelligence—while exploiting the advantage we have of having the GPT family that we can work on top of as well.

Dylan Patel 00:39:45

Say we roll forward seven years, you no longer have access to OpenAI models. What does Microsoft do to make sure they are leading, or have a leading AI lab? Today, OpenAI has developed many of the breakthroughs, whether it be scaling or reasoning. Or Google’s developed all the breakthroughs like transformers.

But it is also a big talent game. You’ve seen Meta spend north of $20 billion on talent. You’ve seen Anthropic poach the entire Blueshift reasoning team from Google last year. You’ve seen Meta poach a large reasoning and post-training team from Google more recently. These sorts of talent wars are very capital intensive. Arguably, if you’re spending $100 billion on infrastructure, you should also spend X amount of money on the people using the infrastructure so that they’re more efficiently making these new breakthroughs.

What confidence can one get that Microsoft will have a team that’s world-class that can make these breakthroughs? Once you decide to turn on the money faucet—you’re being a bit capital efficient right now, which is smart it seems, to not waste money doing duplicative work—but once you decide you need to, how can one say, “Oh yeah, now you can shoot up to the top five model?”

Satya Nadella 00:41:00

At the end of the day, we’re going to build a world-class team and we already have a world-class team that’s beginning to be assembled. We have Mustafa coming in, we have Karen. We have Amar Subramanya who did a lot of the post-training at Gemini 2.5 who’s at Microsoft. Nando, who did a lot of the multimedia work at DeepMind, is there. We’re going to build a world-class team. In fact, later this week even, Mustafa will publish something with a little more clarity on what our lab is going to go do.

The thing that I want the world to know, perhaps, is that we are going to build the infrastructure that will support multiple models. Because from a hyperscale perspective, we want to build the most scaled infrastructure fleet that’s capable of supporting all the models the world needs, whether it’s from open source or obviously from OpenAI and others. That’s one job.

Secondly, in our own model capability, we will absolutely use the OpenAI model in our products and we’ll start building our own model. And we may—like in GitHub Copilot where Anthropic is used—even have other frontier models that are going to be wrapped into our products, as well. I think that’s how each time… At the end of the day, the eval of the product as it meets a particular task or a job is what matters. We’ll start back from there into the vertical integration needed, knowing that as long as you’re serving the market well with the product, you can always cost-optimize.

Dwarkesh Patel 00:42:31

There’s a question going forward. Right now, we have models that have this distinction between training and inference. One could argue that there’s a smaller and smaller difference between the different models. Going forward, if you’re really expecting something like human-level intelligence, humans learn on the job. If you think about your last 30 years, what makes Satya tokens so valuable? It’s the last 30 years of wisdom and experience you’ve gained in Microsoft.

We will eventually have models, if they get to human level, which will have this ability to continuously learn on the job. That will drive so much value to the model company that is ahead, at least in my view, because you have copies of one model broadly deployed through the economy learning how to do every single job. And unlike humans, they can amalgamate their learnings to that model. So there’s this sort of continuous learning exponential feedback loop, which almost looks like a sort of intelligence explosion.

If that happens and Microsoft isn’t the leading model company by that time… You’re saying that well, we substitute one model for another, et cetera. Doesn’t that then matter less? Because it’s like this one model knows how to do every single job in the economy, the others in the long tail don’t.

Satya Nadella 00:43:39

Your point, if there’s one model that is the only model that’s most broadly deployed in the world and it sees all the data and it does continuous learning, that’s game set match and you shut shop. The reality that at least I see is that in the world today, for all the dominance of any one model, that is not the case. Take coding, there are multiple models. In fact, everyday it’s less the case. There is not one model that is getting deployed broadly. There are multiple models that are getting deployed. It’s like databases. It’s always the thing, “Can one database be the one that is just used everywhere?” Except it’s not. There are multiple types of databases that are getting deployed for different use cases.

I think that there are going to be some network effects of continual learning—I call it data liquidity—that any one model has. Is it going to happen in all domains? I don’t think so. Is it going to happen in all geos? I don’t think so. Is it going to happen in all segments? I don’t think so. It’ll happen in all categories at the same time? I don’t think so. So therefore I feel like the design space is so large that there’s plenty of opportunity.

But your fundamental point is having a capability which is at the infrastructure layer, model layer, and at the scaffolding layer, and then being able to compose these things not just as a vertical stack, but to be able to compose each thing for what its purpose is. You can’t build an infrastructure that’s optimized for one model. If you do that, what if you fall behind? In fact, all the infrastructure you built will be a waste. You kind of need to build an infrastructure that’s capable of supporting multiple families and lineages of models. Otherwise the capital you put in, which is optimized for one model architecture, means you’re one tweak away, some MoE-like breakthrough that happens, and your entire network topology goes out of the window. That’s a scary thing.

Therefore you kind of want the infrastructure to support whatever may come in your own model family and other model families. You’ve got to be open. If you’re serious about the hyperscale business, you’ve got to be serious about that. If you’re serious about being a model company, you have to basically say, “What are the ways people can do things on top of the model so that I can have an ISV ecosystem?” Unless I’m thinking I’ll own every category, that just can’t be that. Then you won’t have an API business and that, by definition, will mean you’ll never be a platform company that’s successfully deployed everywhere. Therefore the industry structure is such that it will really force people to specialize. In that specialization, a company like Microsoft should compete in each layer by its merits, but not think that this is all about the road to game set match, where I just compose vertically all these layers. That just doesn’t happen.

00:47:47 - The hyperscale business

Dylan Patel 00:47:47

So last year Microsoft was on path to be the largest infrastructure provider by far. You were the earliest in 2023, so you went out there, you acquired all the resources in terms of leasing data centers, starting construction, securing power, everything. You guys were on pace to beat Amazon in 2026 or 2027. Certainly by 2028 you were going to beat them.

Since then, let’s call it, in the second half of last year, Microsoft did this big pause, where they let go of a bunch of leasing sites that they were going to take, which then Google, Meta, Amazon in some cases, Oracle, took these sites.

We’re sitting in one of the largest data centers in the world, so obviously it’s not everything, you guys are expanding like crazy. But there are sites that you just stopped working on. Why did you do this?

Satya Nadella 00:48:32

This goes back a little bit to, what is the hyperscale business all about? One of the key decisions we made was that if we’re going to build out Azure to be fantastic for all stages of AI—from training to mid-training to data gen to inference—we just need fungibility of the fleet. So that entire thing caused us basically not to go build a whole lot of capacity with a particular set of generations.

Because the other thing you have to realize is that having up to now 10x’ed every 18 months enough training capacity for the various OpenAI models, we realized that the key is to stay on that path. But the more important thing is to have a balance, to not just train, but to be able to serve these models all around the world. Because at the end of the day, the rate of monetization is what will then allow us to keep funding. And then the infrastructure was going to need us to support multiple models.

So once we said that that’s the case, we just course-corrected to the path we’re on. If I look at the path we’re on, we are doing a lot more starts now. We are also buying up as much managed capacity as we can, whether it’s to build, whether it’s to lease, or even GPUs as a service. But we’re building it for where we see the demand and the serving needs and our training needs. We didn’t want to just be a hoster for one company and have just a massive book of business with one customer. That’s not a business, you should be vertically integrated with that company.

Given that OpenAI was going to be a successful independent company, which is fantastic. It makes sense. And even Meta may use third-party capacity, but ultimately they’re all going to be first-party. For anyone who has large scale, they’ll be a hyperscaler on their own. To me, it was to build out a hyperscale fleet and our own research compute. That’s what the adjustment was. So I feel very, very good.

By the way, the other thing is that I didn’t want to get stuck with massive scale of one generation. We just saw the GB200s, the GB300s are coming. By the time I get to Vera Rubin, Vera Rubin Ultra, the data center is going to look very different because the power per rack, power per row, is going to be so different. The cooling requirements are going to be so different. That means I don’t want to just go build out a whole number of gigawatts that are only for a one-generation, one family. So I think the pacing matters, the fungibility and the location matters, the workload diversity matters, customer diversity matters and that’s what we’re building towards.

The other thing that we’ve learned a lot is that every AI workload does require not only the AI accelerator, but it requires a whole lot of other things. In fact, a lot of the margin structure for us will be in those other things. Therefore, we want to build out Azure as being fantastic for the long tail of the workloads, because that’s the hyperscale business, while knowing that we’ve got to be super competitive starting with the bare-metal for the highest end training.

But that can’t crowd out the rest of the business, because we’re not in the business of just doing five contracts with five customers being their bare-metal service. That’s not a Microsoft business. That may be a business for someone else, and that’s a good thing. What we have said is that we’re in the hyperscale business, which is at the end of the day a long tail business for AI workloads. And in order to do that, we will have some leading bare-metal-as-a-service capabilities for a set of models, including our own. And that, I think, is the balance you see.

Dylan Patel 00:52:41

Another question that comes around this whole fungibility topic. Okay, it’s not where you want it, you would rather have it in a good population center, like Atlanta. We’re here. There’s also the question of, how much does that matter as the horizon of AI tasks grows? 30 seconds for a reasoning prompt, or 30 minutes for a deep research, or it’s going to be hours for software agents at some point and days and so on and so forth, the time to human interaction. Why does it matter if it’s location A, B, or C?

Satya Nadella 00:53:14

It’s a great question. That’s exactly it. In fact, that’s one of the other reasons why we want to think about what an Azure region looks like and what is the networking between Azure regions. This is where I think as the model capabilities evolve and the usage of these tokens evolves, whether it’s synchronously or asynchronously, you don’t want to be out of position.

Then on top of that, by the way, what are the data residency laws? There’s the entire EU thing, where we literally had to create an EU Data Boundary. That basically meant that you can’t just roundtrip a call to wherever, even if it’s asynchronous. Therefore you need to have maybe regional things that are high density, and then the power costs and so on.

But you’re 100% right in bringing up that the topology as we build out will have to evolve. One, for tokens per dollar per watt. What are the economics? Overlay that with, what is the usage pattern? Usage pattern in terms of synchronous, asynchronous. But also what is the compute storage? Because the latencies may matter for certain things. The storage better be there. If I have a Cosmos DB close to this for session data or even for an autonomous thing, then that also has to be somewhere close to it, and so on. All of those considerations are what will shape the hyperscale business.

Dylan Patel 00:54:38

Prior to the pause, what we had forecasted for you, by 2028 you were going to be 12–13 gigawatts. Now we’re at nine and a half or so.

But something that’s even more relevant—and I just want you to more concretely state that this is the business you don’t want to be in—is that Oracle’s going from 1/5th your size to bigger than you by the end of 2027.

While it’s not a Microsoft-level quality of return on invested capital, they’re still making 35% gross margins. So the question is, maybe it’s not Microsoft’s business to do this, but you’ve created a hyperscaler now by refusing this business, by giving away the right of first refusal, et cetera.

Satya Nadella 00:55:23

First of all, I don’t want to take away anything from the success Oracle has had in building their business and I wish them well. The thing that I think I’ve answered for you is that it didn’t make sense for us to go be a hoster for one model company with limited time horizon RPO. Let’s just put it that way.

The thing that you have to think through is not what you do in the next five years, but what you do for the next 50. We made our set of decisions. I feel very good about our OpenAI partnership and what we’re doing. We have a decent book of business. We wish them a lot of success. In fact, we are buyers of Oracle capacity. We wish them success.

But at this point, I think the industrial logic for what we are trying to do is pretty clear, which is that it’s not about chasing… First of all, I track, by the way, your things whether it’s AWS or Google and ours, which I think is super useful. But it doesn’t mean I have to chase those. I have to chase them for not just the gross margin that they may represent in a period of time. What is this book of business that Microsoft uniquely can go clear, which makes sense for us to clear? That’s what we’ll do.

Dwarkesh Patel 00:56:40

I have a question even stepping back from this, I take your point that it’s a better business to be in, all else equal, to have a long tail of customers you can have higher margin from rather than serving bare metal to a few labs. But then there’s a question of, which way is the industry evolving? If we believe we’re on the path to smarter and smarter AIs, then why isn’t the shape of the industry that the OpenAIs and Anthropics and DeepMinds are the platform on which the long tail of enterprises are actually doing business? They need bare metal, but they are the platform. What is the long tail that is directly using Azure? Because you want to use the general cognitive core.

Satya Nadella 00:57:22

But those models are all going to be available on Azure, so any workload that says, “Hey, I want to use some open source model and an OpenAI model,” if you go to Azure Foundry today, you have all these models that you can provision, buy PTUs, get a Cosmos DB, get a SQL DB, get some storage, get some compute. That’s what a real workload looks like. A real workload is not just an API call to a model. A real workload needs all of these things to go build an app or instantiate an application.

In fact, the model companies need that to build anything. It’s not just like, “I have a token factory.” I have to have all of these things. That’s the hyperscale business. And it’s not on any one model, but all of these models. So if you want Grok plus, say, OpenAI plus an open source model, come to Azure Foundry, provision them, build your application. Here is a database. That’s kind of what the business is.

There is a separate business called just selling raw bare-metal services to model companies. And that’s the argument about how much of that business you want to be in and not be in and what that is. It’s a very different segment of the business, which we are in, and we also have limits to how much of it is going to crowd out the rest of it. But that’s kind of at least the way I look at it.

Dylan Patel 00:58:40

There are sort of two questions here. One is, why couldn’t you just do both? The other one is, given our estimates on what your capacity is in 2028, it’s three and a half gigawatts lower. Sure, you could have dedicated that to OpenAI training and inference capacity, but you could have also dedicated that to actually just running Azure, running Microsoft 365, running GitHub Copilot. I could have just built it and not given it to OpenAI.

Satya Nadella 00:59:08

Or I may want to build it in a different location. I may want to build it in the UAE, I may want to build it in India, I may want to build it in Europe. One of the things is, as I said, where we have real capacity constraints right now, given the regulatory needs and the data sovereignty needs, we’ve got to build all over the world. First of all, stateside capacity is super important, and we want to build everything.

But when I look out to 2030, I have a global view of what is Microsoft’s shape of business by first-party and third-party. Third-party segmented by the frontier labs and how much they want versus the inference capacity we want to build for multiple models, and our own research compute needs. That’s all going into my calculus. You’re rightfully pointing out the pause, but the pause was not done because we said, “Oh my God, we don’t want to build that.” We realized that we want to build what we want to build slightly differently by both workload type as well as geo-type and timing as well.

We’ll keep ramping up our gigawatts, and the question is at what pace and in what location. And how do I ride Moore’s law on it, which is, do I really want to overbuild three and a half in 2027 or do I want to spread that in 2027-28 knowing even… One of the biggest learnings we had even with Nvidia is that their pace increased in terms of their migrations.

That was a big factor. I didn’t want to go get stuck for four or five years of depreciation on one generation. In fact, Jensen’s advice to me was two things. One is, get on the speed-of-light execution. That’s why the execution in this Atlanta data center.... I mean, it’s like 90 days between when we get it and to hand off to a real workload. That’s real speed-of-light execution on that front. I wanted to get good on that.

And then that way I’m building each generation in scaling. And then every five years, you have something much more balanced. So it becomes literally like a flow for a large-scale industrial operation like this where you’re suddenly not lopsided, where you’ve built up a lot in one time and then you take a massive hiatus because you’re stuck with all this, to your point, in one location which may be great for training, or it may not be great for inference because I can’t serve, even if it’s all asynchronous, because Europe won’t let me round-trip to Texas. So that’s all of the things.

Dylan Patel 01:01:38

How do I rationalize this statement with what you’ve done over the last few weeks? You’ve announced deals with Iris Energy, with Nebius, and Lambda Labs, and there’s a few more coming as well. You’re going out there and securing capacity that you’re renting from the neoclouds rather than having built it yourself.

Satya Nadella 01:01:58

It’s fine for us because now when you have line of sight to demand, which can be served where people are building, it’s great. In fact we will take leases, we will take build-to-suit, we’ll even take GPUs-as-a-service where we don’t have capacity but we need capacity and someone else has that.

And by the way, I would even sort of welcome every neocloud to just be part of our marketplace. Because guess what? If they go bring their capacity into our marketplace, that customer who comes through Azure will use the neocloud, which is a great win for them, and will use compute, storage, databases, all the rest from Azure. So I’m not at all thinking of this as, “Hey, I should just go gobble up all of that myself.”

01:02:44 - In-house chip & OpenAI partnership

Dwarkesh Patel 01:02:44

You mentioned how this depreciating asset, in five or six years, is 75% of the TCO of a data center. And Jensen is taking a 75% margin on that. So what all the hyperscalers are trying to do is develop their own accelerator so that they can reduce this overwhelming cost for equipment, to increase their margins.

Dylan Patel 01:03:09

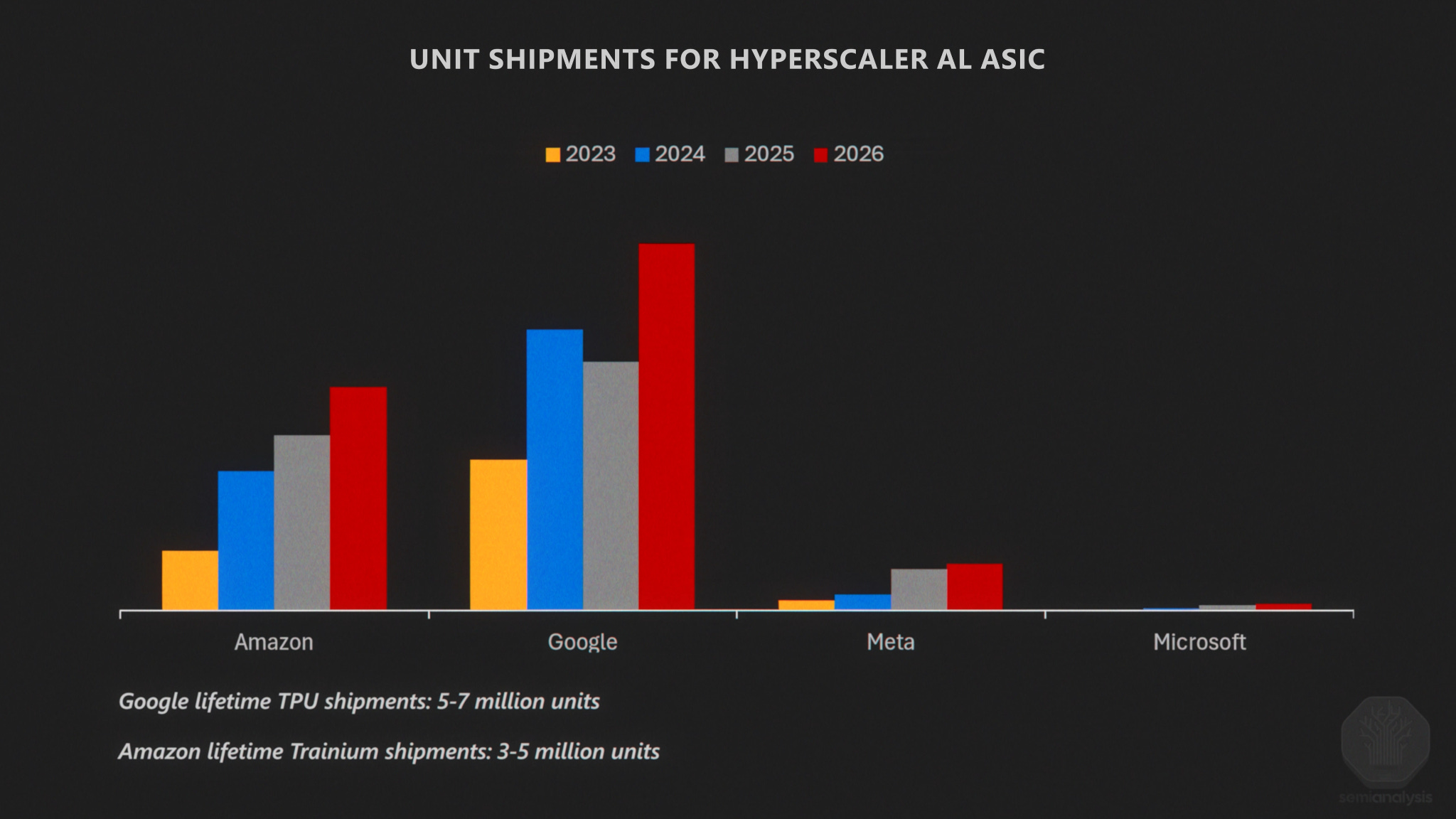

And when you look at where they are, Google’s way ahead of everyone else. They’ve been doing it for the longest.

They’re going to make something like five to seven million chips of their own TPUs. You look at Amazon and they’re trying to make three to five million [Lifetime shipment units]. But when we look at what Microsoft is ordering of their own chips, it’s way below that number. You’ve had a program for just as long. What’s going on with your internal chips?

Satya Nadella 01:03:32

It’s a good question. A couple of things. One is that the thing that is the biggest competitor for any new accelerator is kind of even the previous generation of Nvidia. In a fleet, what I’m going to look at is the overall TCO. The bar I have, even for our own… By the way, I was just looking at the data for Maia 200 which looks great, except that one of the things that we learned even on the compute side… We had a lot of Intel, then we introduced AMD, and then we introduced Cobalt. That’s how we scaled it. We have good existence proof of, at least in core compute, how to build your own silicon and then manage a fleet where all three are at play in some balance.

Because by the way, even Google’s buying Nvidia, and so is Amazon. It makes sense because Nvidia is innovating and it’s the general-purpose thing. All models run on it and customer demand is there. Because if you build your own vertical thing, you better have your own model, which is either going to use it for training or inference, and you have to generate your own demand for it or subsidize the demand for it. So therefore you want to make sure you scale it appropriately.

The way we are going to do it is to have a close loop between our own MAI models and our silicon, because I feel like that’s what gives you the birthright to do your own silicon, where you literally have designed the microarchitecture with what you’re doing, and then you keep pace with your own models. In our case, the good news here is that OpenAI has a program which we have access to. So therefore to think that Microsoft is not going to have something that’s—

Dylan Patel 01:05:15

What level of access do you have to that?

Satya Nadella 01:05:16

All of it.

Dylan Patel 01:05:17

You just get the IP for all of that? So the only IP you don’t have is consumer hardware?

Satya Nadella 01:05:20

That’s it.

Dylan Patel 01:05:21

Oh, okay. Interesting.

Satya Nadella 01:05:26

By the way, we gave them a bunch of IP as well to bootstrap them. This is one of the reasons why they… Because we built all these supercomputers together. We built it for them and they benefited from it, rightfully so. And now as they innovate, even at the system level, we get access to all of it. And we first want to instantiate what they build, for them, but then we’ll extend it.

So if anything, the way I think about your question is, Microsoft wants to be a fantastic, I’ll call it, speed-of-light execution partner for Nvidia. Because quite frankly that fleet is life itself. Obviously Jensen’s doing super well with his margins, but the TCO has many dimensions to it and I want to be great at that TCO. On top of that, I want to be able to really work with the OpenAI lineage and the MAI lineage and the system design, knowing that we have the IP rights on both ends.

Dwarkesh Patel 01:06:32

Speaking of rights, you had an interview a couple days ago where you said that in the new agreement you made with OpenAI you have rights, the exclusivity, to the stateless API calls that OpenAI makes. We were sort of confused about if there’s any state whatsoever. You were just mentioning a second ago that all these complicated workloads that are coming up are going to require memory and databases and storage and so forth. Is that now not stateless if ChatGPT is storing stuff on sessions?

Satya Nadella 01:07:03

That’s the reason why. The strategic decision we made, and also accommodating for the flexibility OpenAI needed in order to be able to procure compute for… Essentially think of OpenAI having a PaaS business and a SaaS business. The SaaS business is ChatGPT. Their PaaS business is their API. That API is Azure-exclusive. The SaaS business, they can run it anywhere.

Dylan Patel 01:07:31

And they can partner with anyone they want to to build SaaS products?

Satya Nadella 01:07:34

If they want a partner and that partner wants to use a stateless API, then Azure is the place where they can get the stateless API.

Dylan Patel 01:07:43

It seems like there’s a way for them to build the product together and it’s a stateful thing…

Satya Nadella 01:07:47

No, for even that they’ll have to come to Azure. Again, this is done in the spirit of “what is it that we value as part of our partnership.” And we made sure that, at the same time, we were good partners to OpenAI given all the flexibility they needed.

Dylan Patel 01:08:05

So for example, Salesforce wants to integrate OpenAI. It’s not through an API. They actually work together, train a model together and deploy it on, let’s say, Amazon now. Is that allowed or do they have to use your…

Satya Nadella 01:08:16

For any custom agreement like that, they will have to come run it… There are some few exceptions, the US government and so on, that we made, but other than that, they’d have to come to Azure.

01:09:35 - The CAPEX explosion

Dwarkesh Patel 01:09:35

Stepping back, when we were walking back and forth through the factory, one of the things you were talking about is that Microsoft, you can think of it as a software business, but now it’s really becoming an industrial business. There’s all this capex, there’s all this construction. If you just look over the last two years, your capex has sort of tripled. Maybe you extrapolate that forward, it actually just becomes this huge industrial explosion.

Dylan Patel 01:10:01

Other hyperscalers are taking loans. Meta has done a $20 billion loan at Louisiana. They’ve done a corporate loan. It seems clear everyone’s free cash flow is going to zero, which I’m sure Amy is going to beat you up if you even try to do that, but what’s happening?

Satya Nadella 01:10:19

I think the structural change is what you’re referencing, which is massive. I describe it as we are now a capital-intensive business and a knowledge-intensive business. In fact, we have to use our knowledge to increase the ROIC on the capital spend.

The hardware guys have done a great job of marketing Moore’s Law, which I think is unbelievable and it’s great. But if you even look at some of the stats I even did in my earnings call, for a given GPT family, the software improvements of really throughput in terms of tokens-per-dollar-per-watt that we’re able to get quarter-over-quarter, year-over-year, it’s massive. It’s 5x, 10x, maybe 40x in some of these cases, just because of how you can optimize. That’s knowledge intensity coming to bring out capital efficiency. That, at some level, is what we have to master.

Some people ask me, what is the difference between a classic old-time hoster and a hyperscaler? Software. Yes, it is capital intensive, but as long as you have systems know-how, software capability to optimize by workload, by fleet... That’s why when we say fungibility, there’s so much software in it. It’s not just about the fleet.

It’s the ability to evict a workload and then schedule another workload. Can I manage that algorithm of scheduling around? That is the type of stuff that we have to be world-class at. So yes, I think we’ll still remain a software company, but yes, this is a different business and we’re going to manage. At the end of the day, the cash flow that Microsoft has allows us to have both these arms firing well.

Dwarkesh Patel 01:12:18

It seems like in the short term you have more credence on things taking a while, being more jagged. But maybe in the long term you think the people who talk about AGI and ASI are correct. Sam will be right, eventually.

I have a broader question about what makes sense for a hyperscaler to do, given that you have to invest massively in this thing which depreciates over five years. So if you have 2040 timelines to the kind of thing that somebody like Sam anticipates in three years, what is a reasonable thing for you to do in that world?

Satya Nadella 01:12:52

There needs to be an allocation to, I’ll call it, research compute. That needs to be done like you did R&D. That’s the best way to even account for it, quite frankly. We should think of it as just R&D expense and you should say, “What’s the research compute and how do you want to scale it?” Let’s even say it’s an order of magnitude scale in some period. Pick your thing, is it two years? Is it 16 months? What have you. That’s sort of one piece, which is table stakes, that’s R&D expenses.

The rest is all demand driven. Ultimately, you’re allowed to build ahead of demand, but you better have a demand plan that doesn’t go completely off kilter.

Dwarkesh Patel 01:13:39

Do you buy… These labs are now projecting revenues of $100 billion in 2027–28 and they’re projecting revenue to keep growing at this rate of 3x, 2x a year…

Satya Nadella 01:13:50

In the marketplace there’s all kinds of incentives right now, and rightfully so. What do you expect an independent lab that is sort of trying to raise money to do? They have to put some numbers out there such that they can actually go raise money so that they can pay their bills for compute and what have you.

And it’s a good thing. Someone’s going to take some risk and put it in there, and they’ve shown traction. It’s not like it’s all risk without seeing the fact that they’ve been performing, whether it’s OpenAI, or whether it’s Anthropic. So I feel great about what they’ve done, and we have a massive book of business with these chaps. So therefore that’s all good.

But overall ultimately, there’s two simple things. One is you have to allocate for R&D. You brought up talent. The talent for AI is at a premium. You have to spend there. You’ve got to spend on compute. So in some sense researcher-to-GPU ratios have to be high. That is sort of what it takes to be a leading R&D company in this world. And that’s something that needs to scale, and you have to have a balance sheet that allows you to scale that long before it’s conventional wisdom and so on. That’s kind of one thing. But the other is all about knowing how to forecast.

01:15:07 - Will the world trust US companies to lead AI?

Dylan Patel 01:15:07

As we look across the world, America has dominated many tech stacks. The US owns Windows through Microsoft, which is deployed even in China, that’s the main operating system. Of course, there’s Linux, which is open source, but Windows is deployed everywhere in China on personal computers. You look at Word, it’s deployed everywhere. You look at all these various technologies, it’s deployed everywhere. And Microsoft and other companies have grown elsewhere. They’re building data centers in Europe and in India and in all these other places, in Southeast Asia and LatAm and Africa. In all of these different places, you’re building capacity.

But this seems quite different. Today, the political aspect of technology, of compute… The US administration didn’t care about the dot-com bubble. It seems like the US administration, as well as every other administration around the world, cares a lot about AI. The question is, we’re sort of in a bipolar world, at least with the US and China, but Europe and India and all these other countries are saying, “No, we’re going to have sovereign AI as well.”

How does Microsoft navigate the difference to the 90s—where there’s one country in the world that matters, it’s America, and our companies sell everywhere and therefore Microsoft benefits massively—to a world where it is bipolar? Where Microsoft can’t just necessarily have the right to win all of Europe or India or Singapore. There are actually sovereign AI efforts. What is your thought process here and how do you think about this?

Satya Nadella 01:16:36

It’s a super critical piece. I think that the key, key priority for the US tech sector and the US government is to ensure that we not only do leading innovative work, but that we also collectively build trust around the world on our tech stack. Because I always say the United States is just an unbelievable place. It’s just unique in history. It’s 4% of the world’s population, 25% of the GDP, and 50% of the market cap. I think you should think about those ratios and reflect on it.

That 50% happens because quite frankly the trust the world has in the United States, whether it’s its capital markets or whether it’s its technology and its stewardship of what matters at any given time in terms of leading sector. If that is broken, then that’s not a good day for the United States. We start with that, which I think President Trump gets, the White House, David Sacks, everyone really, I think, gets it.

So therefore I applaud anything that the United States government and the tech sector jointly does to, for example, put our own capital at risk, collectively as an industry, in every part of the world. I would like the USG to take credit for foreign direct investment by American companies all over the world. It’s the least talked about, but the best marketing that the United States should be doing is that it’s not just about all the foreign direct investment coming into the United States, but the most leading sector, which is these AI factories, are all being created all over the world. By whom? By America and American companies.

And so you start there, and then you even build other agreements around it, which are around their continuity, their legitimate sovereignty concerns, around whether it’s data residency, for them to have real agency and guarantees on privacy, and so on. In fact, our European commitments are worth reading. We made a series of commitments to Europe on how we will govern our hyperscale investment there such that the European Union and the European countries have sovereignty.

We’re also building sovereign clouds in France and in Germany. We have something called Sovereign Services on Azure, which literally gives people key management services along with confidential computing, including confidential computing in GPUs, which we’ve done great innovative work with Nvidia. So I feel very, very good about being able to build, both technically and through policy, this trust in the American tech stack.

Dwarkesh Patel 01:19:42

How do you see this shaking out as you have this network effect with continual learning and things on the model level? Maybe you have equivalent things at the hyperscaler level as well. Do you expect that the countries will say, “Look, it’s clear one model or a couple models are the best, and so we’re going to use them, but we’re going to have some laws around the weights having to be hosted in our country”? Or do you expect that there will be this push so that it has to be a model trained in our country?

Maybe an analogy here is that semiconductors are very important to the economy, and people would like to have their sovereign semiconductors, but TSMC is just better. And semiconductors are so important to the economy that you will just go to Taiwan and buy the semiconductors. You have to. Will it be like that with AI?

Satya Nadella 01:20:26

Ultimately, what matters is the use of AI in their economy to create economic value. That’s the diffusion theory, which ultimately, it’s not the leading sector, but it’s the ability to use the leading technology to create your own comparative advantage. So I think that will fundamentally be the core driver.

But that said, they will want continuity of that. So in some sense, that’s one of the reasons why, I believe, there’s always going to be a check to “Hey, can this one model have all the runaway deployment?” That’s why open source is always going to be there. There will be, by definition, multiple models. That’ll be one way. That’s one way for people to sort of demand continuity and not have concentration risk, that’s another way to say it.

And so you say, “Hey, I want multiple models, and then I want an open source.” I feel that as long as that’s there, every country will feel like, “Okay, I don’t have to worry about deploying the best model and broadly diffusing because I can always take what is my data and my liquidity and move it to another model, whether it’s open source or from another country or what have you.” Concentration risk and sovereignty, which is really agency, those are the two things that will drive the market structure.

Dylan Patel 01:21:49

The thing about this is that this doesn’t exist for semiconductors. All refrigerators, cars have chips made in Taiwan.

Satya Nadella 01:21:56

It didn’t exist until now.

Dylan Patel 01:22:00